Rising Prices, Falling Confidence: Managing Household Budgets During Middle-East Turmoil

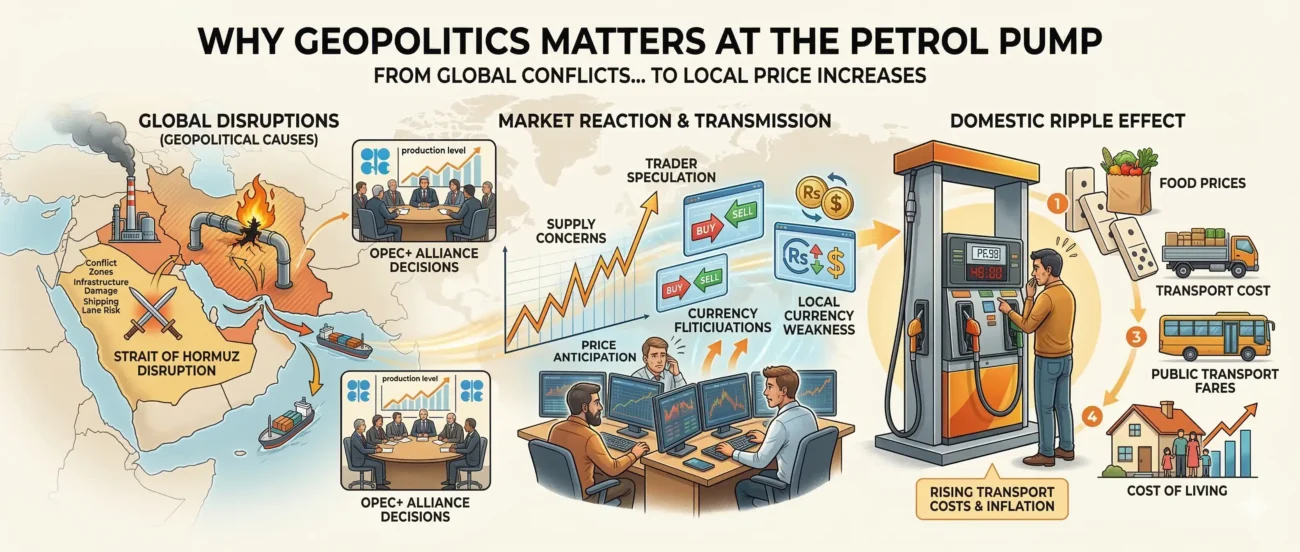

The world feels more uncertain than ever right now. The ongoing war in the Middle East—sparked by US and Israeli strikes on Iran starting February 28, 2026—has escalated quickly. It has already led to massive air campaigns, retaliatory missile and drone attacks across the region (including Qatar, Saudi Arabia, and the UAE), strikes on energy facilities, and disruptions in the Strait of Hormuz. This key shipping route handles a 20% of the world’s oil and gas, and attacks plus partial blockages have caused global oil prices to surge sharply—hovering well above $100-110 per barrel in recent weeks, with spikes even higher during intense phases.

The ongoing war is no longer just a distant geopolitical issue—it is directly affecting household budgets, especially in countries like Pakistan. For us, this is a serious concern because Pakistan imports most of its fuel, making it highly vulnerable to global price shocks.

The result is already visible: rising petrol prices, higher transport fares, and growing uncertainty about the future.

This blog explains what is happening—and more importantly, how households can manage their finances during this crisis.

How the Iran Crisis Is Affecting Your Daily Expenses

The impact is not abstract—it is immediate and practical:

- Fuel prices are rising → Transport and commuting costs increase

- Food prices are increasing → Higher transport and import costs raise grocery bills

- Electricity and gas may become expensive → Energy shortages push tariffs upward

- General inflation is expected to rise → It could reach 15–17% in a severe scenario ()

Even small increases in oil prices can significantly raise Pakistan’s import bill and weaken the economy. In simple terms, life is becoming more expensive, and uncertainty is growing.

You can manage your finances by taking the following steps:

-

Rethink Your Monthly Budget Immediately

In normal times, budgeting is important. In a crisis, it becomes essential. Start by listing monthly income, fixed expenses (rent, school fees, utilities), variable expenses (food, fuel, shopping)

Now adjust your budget based on new realities, not old habits. Fuel and food will likely take a larger share of your income in the coming months.

-

Cut Fuel and Transport Costs

Since the crisis is caused by rising oil prices, savings are most important. Reduce unnecessary travel, prefer carpooling or public transport, combine multiple errands into one trip, and consider remote work options if available. The government has already taken precautionary measures to deal with the situation. Follow the government’s instructions in this regard.

Even small reductions in fuel use can protect your budget.

-

Control Food Spending Strategically

Food inflation often follows fuel inflation. Take practical steps by shifting from branded to local alternatives, buying essential items in bulk before further price hikes, reducing food waste at home, and limiting eating out and takeaway orders.

This is not about deprivation—it is about smart adjustment.

-

Prepare for Utility Bill Increases

Electricity and gas costs often rise after energy shocks. You are advised to use energy-efficient appliances, turn off unused lights and fans, avoid excessive use of heaters or AC, and monitor your monthly units carefully.

Lower consumption today prevents financial pressure tomorrow.

-

Build a Crisis Buffer (Emergency Fund)

This crisis may not end quickly. If the Strait of Hormuz remains disrupted, the impact could last months. Try to save even a small fixed amount each month and keep cash reserves for at least 1–2 months of expenses initially.

In uncertain times, liquidity is more important than luxury.

-

Avoid New Debt—Especially for Consumption

With rising inflation and interest rates, borrowing becomes more dangerous. Avoid taking loans for non-essential spending, do not rely on credit cards for daily expenses, and focus on reducing existing debt.

Debt during inflation can trap households in long-term financial stress.

-

Secure Your Income Sources

Economic uncertainty can affect jobs and businesses. Strengthen your primary income source, explore side income opportunities, and build skills that can generate additional earnings.

Even a small extra income can offset rising costs.

-

Stay Informed—but Don’t Panic

News about war, oil prices, and inflation can create anxiety. But panic decisions—like hoarding or overspending—can worsen your situation. Instead, follow credible updates, adjust your budget gradually, and focus on what you can control.

Financial confidence comes from preparation, not prediction.

Final Thoughts

The Iran–Middle East crisis has shown how global events can quickly affect everyday life. For Pakistan, where fuel imports are essential, the impact is even stronger. Rising prices may be unavoidable—but financial stress is not.

Households that adapt early—by controlling spending, saving wisely, and planning—will be in a much stronger position to face the coming months. In times like these, smart financial decisions are not just helpful—they are necessary for stability and peace of mind.

Leave a comment